Something has got to give

The Federal Reserve has in the past six weeks diligently stuck to its “patience until substantial further progress is seen” monetary policy mantra. Its “reward” has been range-bound US Treasury yields, a slowly depreciating Dollar and a metronomic rise in US equity indices, with all three financial markets exhibiting only modest volatility.

Since 19th April the Dollar NEER has depreciated a further 0.6% to within striking distance of a 14-week low, in line with “our core scenario that the Dollar will indeed lose further ground”. We remain bearish the US Dollar, a theme we will explore in greater detail in forthcoming FIRMS reports.

Fed Chairperson Powell would argue that keeping US Treasury yields in check has been a worthy achievement given the backdrop of President Biden’s ambitious fiscal stimulus plans and accelerating US economic growth and rising domestic and global inflation.

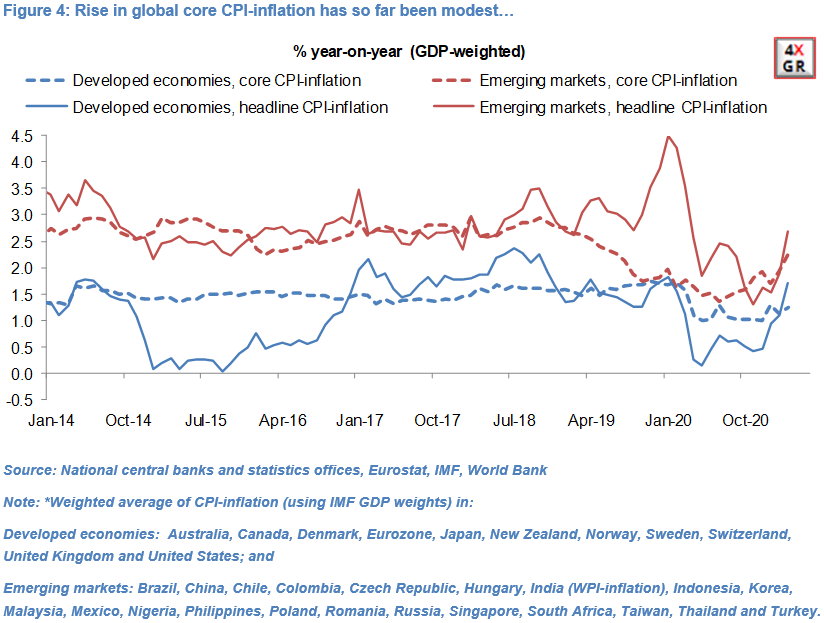

A GDP-weighted measure of headline CPI-inflation in 32 major economies rose to 2.1% yoy in March from 1.4% yoy in February, the largest monthly increase since December 2009. But core CPI-inflation in developed economies rose only marginally in Q1 2021, with the rate of inflation in March of 1.2% yoy below its 10-year average of 1.5% yoy.

While backward looking these data they may explain in part why developed central banks, with the exception of Bank of Canada, have so far felt justified in keeping their policy rates on hold and the modalities of their asset-purchase programs broadly unchanged.

In the past month currencies in Emerging Europe, Africa and Latin America have been main beneficiaries of still reasonably low US yields, weakening Dollar, burgeoning global growth and robust risk appetite. The timing of this EM rebound has coincided with our forecasts.

Non-Japan Asian currencies have lagged, which we attribute in part to portfolio outflows and NJA central banks keeping a close eye on a flat-lining Chinese Renminbi.

This differentiated EM currency rally will extend near-term, in our view, but high-yielding EM currencies in particular remain vulnerable to any spikes in US and other developed market government bond yields and more generally market volatility.

Read the full article here

Olivier is an economist and rates & FX strategist with over 22 years experience in financial markets. He is Director and Founder of 4X Global Research, an independent, London-based consultancy which provides institutional and corporate clients with substantive research, high-quality analysis and insight on emerging and G20 economies and financial markets.