Fed hikes not immune from equity collapse

The Fed is widely expected to hike its policy rate 25bp to 0.25-0.50% (its first since December 2018) at its meeting on 16th March, by which point it is due to have ended its asset purchases. Some FOMC members will likely push for a larger 50bp hike.

Markets, as of 4th February, were pricing in a total of 120bp hikes in 2022, up from 117bp as of 28th January. In line with our forecast 2-year US Treasury yields have risen to their high since January 2020, albeit with regular and sometimes sizeable pull-backs.

US macro indicators, including ISM PMI figures, suggest that US economic growth slowed in January. However, the labour market remained strong and core PCE inflation rose to 4.9% yoy in December or more than twice the Fed’s long-term target of 2%.

While cost-push pressures, including rising energy prices, supply-side shortages and bottlenecks and higher freight prices, have clearly contributed to higher PCE-inflation, so have demand-pull pressures, with personal expenditure back on trend since Q4 2021. This is not the case in the United Kingdom, in our view, and Bank of England policy rate hikes (50bp so far in this cycle) will do more harm than good to the UK economy.

The S&P 500’s sell-off in January and 2.4% fall on 3rd February give food for thought as to whether successive Fed hikes will eventually collapse US equities and the implications for the Dollar. The S&P 500 and Dollar NEER were inversely correlated in the first 15 months of the pandemic but have since mid-June 2021 trended in the same direction.

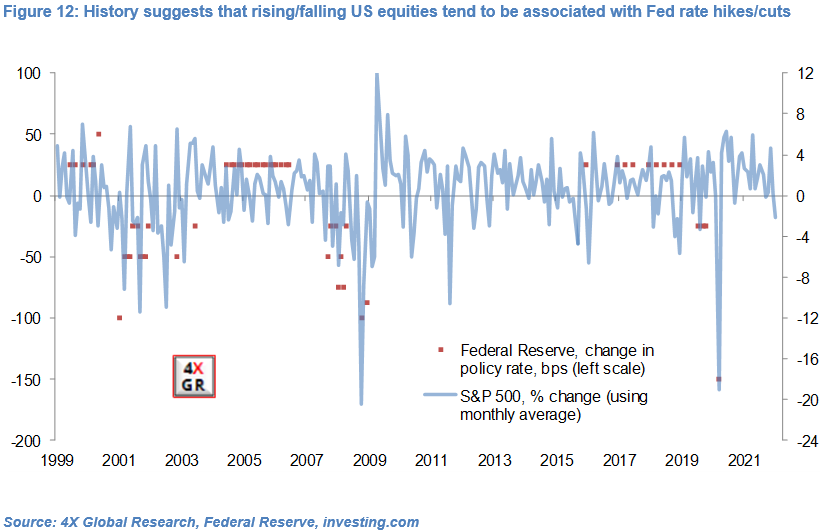

The other question is how the Fed would react should US equities rapidly trend lower. Our analysis shows a strong, positive historical correlation between disposable income, US consumer confidence, households’ net-worth (including equity holdings), and personal consumption expenditure. Moreover, the past three Fed hiking cycles (1999-2000, 2004-2006 and 2016-2018) were all associated with robust US equities.

Of course “this time is different”, with the Fed’s real policy rate at a record-low. However, we think the direction of US equities, and their impact on consumption and ultimately inflation, will colour the timing and magnitude of Fed rate hikes and the management of its balance sheet. Just don’t expect the Fed to admit as much.

Read the full article here

Olivier is an economist and rates & FX strategist with over 22 years experience in financial markets. He is Director and Founder of 4X Global Research, an independent, London-based consultancy which provides institutional and corporate clients with substantive research, high-quality analysis and insight on emerging and G20 economies and financial markets.