Light at the end of long Eurozone tunnel?

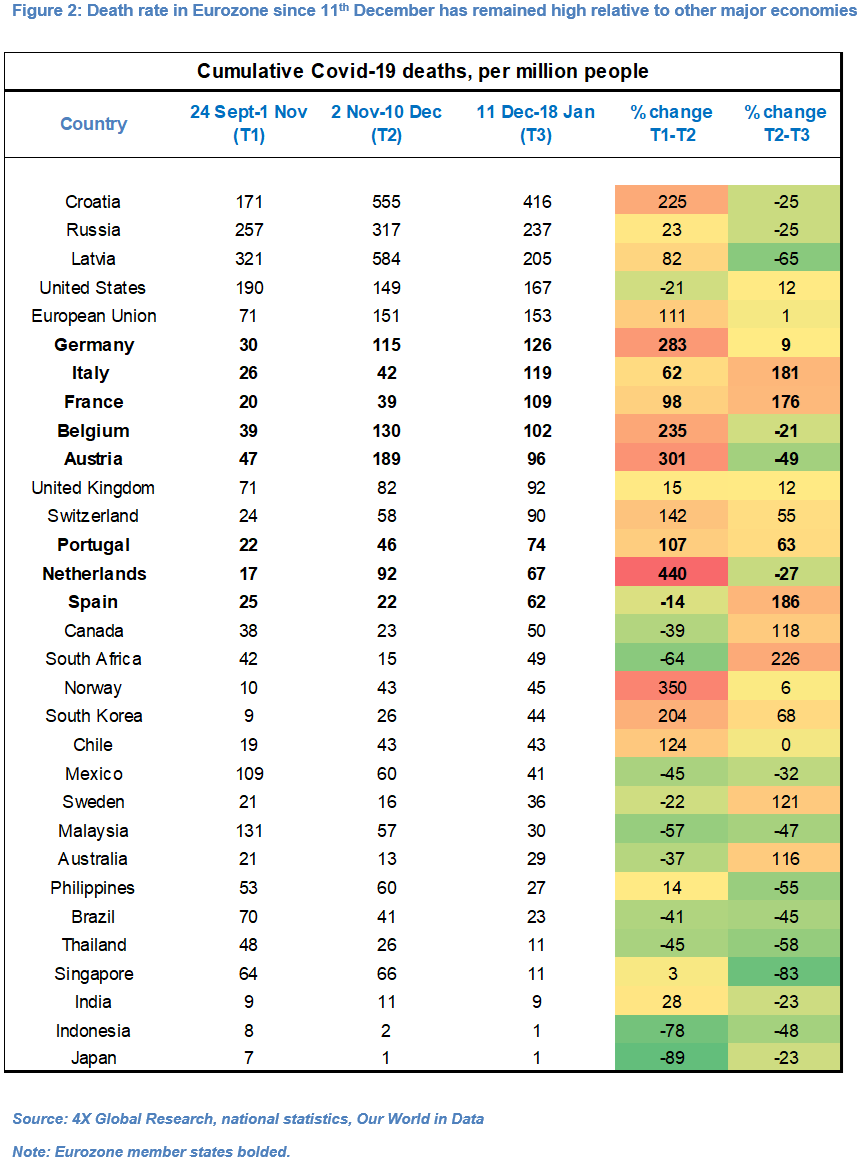

The number of new daily cases of Covid-19 has remained at or near record-highs in most Eurozone countries, including Germany, France, Italy and Spain, and the number of deaths since 11th December has either risen materially from the previous corresponding period, albeit from low levels (France, Italy, Portugal and Spain), or been broadly stable (Germany).

The majority of Eurozone governments, in a bid to protect health systems, have therefore on the whole adopted a conservative path of least regret in the past six weeks and either maintained or in some cases even intensified strict social distancing measures and travel restrictions, in line with our forecast.

Nevertheless, death rates have remained well below the Delta peaks and have in the past five weeks fallen in Austria, Belgium and the Netherlands. Moreover, the United Kingdom, where Covid-19 case numbers started to fall sharply about three weeks ago, could provide a template for how things unfold in Eurozone countries, in our view.

The British government on 19th January announced that it would scrap next week the already light “Plan B” restrictions introduced in England in December. It is also expected to further ease travel rules and restrictions on care home visits and could end, potentially before 24th March, the legal requirement for people who test positive to self-isolate.

Our core scenario is that case numbers will start to fall across the Eurozone in the coming month and that, with a lag, death rates will start to decline and governments will follow the UK’s lead and gradually roll back social distancing measures and travel restrictions. French PM Castex last night announced an easing of domestic rules as of 2nd February.

However, based on precedent, Eurozone governments are still likely to maintain stricter social distancing measures than the more laissez-faire British government. These measures, which in many Eurozone countries pre-date the WHO classifying Omicron as a “strain of concern” on 26th November 2021, will likely continue to weigh on economic growth near-term, as argued in “Don’t forget Delta” (9th December 2021).

We see further Euro weakness in weeks ahead, including against Sterling, but (cheap) valuations and (light) market positioning may eventually favour the Eurozone currency.

Read the full article here

Olivier is an economist and rates & FX strategist with over 22 years experience in financial markets. He is Director and Founder of 4X Global Research, an independent, London-based consultancy which provides institutional and corporate clients with substantive research, high-quality analysis and insight on emerging and G20 economies and financial markets.