Political data point to Macron winning French presidential election – question is by what margin

Five years ago we wrote a comprehensive four-part guide to the 2017 French Presidential (and legislative) elections. It allied a qualitative breakdown of presidential candidates’ political bias and policy agendas to a detailed statistical analysis of the previous eight presidential elections (47 years of political data).

We found a number of robust statistical relationships, including (contrary to popular belief) the reliability of opinion polls in “predicting” presidential elections. These underpinned our accurate and arguably non-consensus forecasts that Emmanuel Macron and Marine Le Pen would top the first round and that Macron would comfortably win the second round to become President, which would in turn contribute to the Euro’s further appreciation.

We have updated our analysis ahead of the first and second rounds of the 2022 election on respectively 10th and 24th April and the legislative elections in June.

The Republican Party’s Valérie Pécresse and far-right candidate Charles Zeymour (both contesting their first presidential election), Covid-19, the cost of living crunch in France and current geopolitical turmoil have muddied political waters.

However, our core scenario is that centre-right President Macron, who is toping first round opinion polls (with 27-28%), will comfortably make it to the second round.

Macron, who is also leading head-to-head opinion polls for the second round, would beat either the far-right’s Marine Le Pen (as he did in 2017 by two votes to one) or the far-left’s Jean-Luc Mélenchon to secure the presidency. But Macron’s margin of victory will likely be smaller than in 2017, whether he faces off Le Pen or Mélenchon, based on opinion polls.

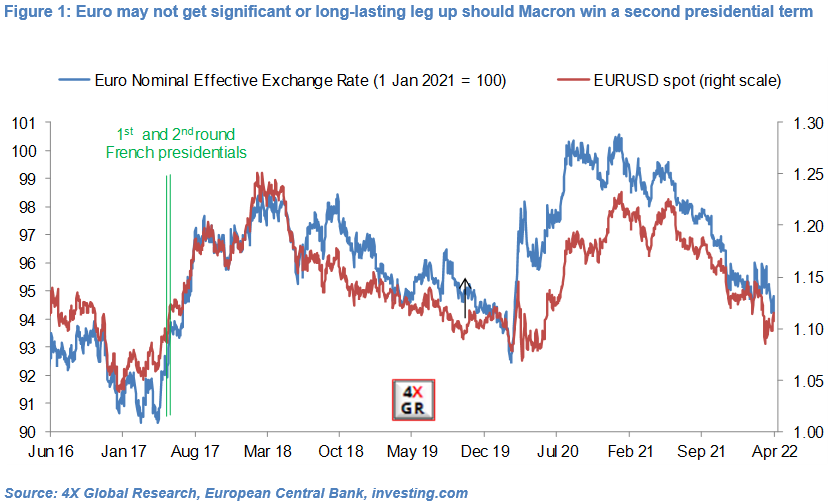

Euro may not get much of a leg-up this time round. Macron is more of a shoe-in to win than in 2017 and concerns about nationalist and far-right parties acceding to power in Europe less acute than in 2016-2017. Moreover, the Euro is facing a number of headwinds, including still very loose ECB monetary policy and Eurozone’s dependence on fossil fuel supplies from Russia. Similarly, should Macron win a second term, we think that any relief rally in French and Eurozone equity markets is likely to be modest and short-lived.

Read the full article here

Olivier is an economist and rates & FX strategist with over 22 years experience in financial markets. He is Director and Founder of 4X Global Research, an independent, London-based consultancy which provides institutional and corporate clients with substantive research, high-quality analysis and insight on emerging and G20 economies and financial markets.