Emerging Market currencies: Hopes and Realities

Media coverage of Emerging Market currencies tends to oscillate between the very bearish and very bullish, with little differentiation between low and high-yielding currencies or between regional blocks let alone between the dozens of currencies still referred to, rightly or wrongly, as “emerging”. Price action in 2019 only partially vindicates this approach.

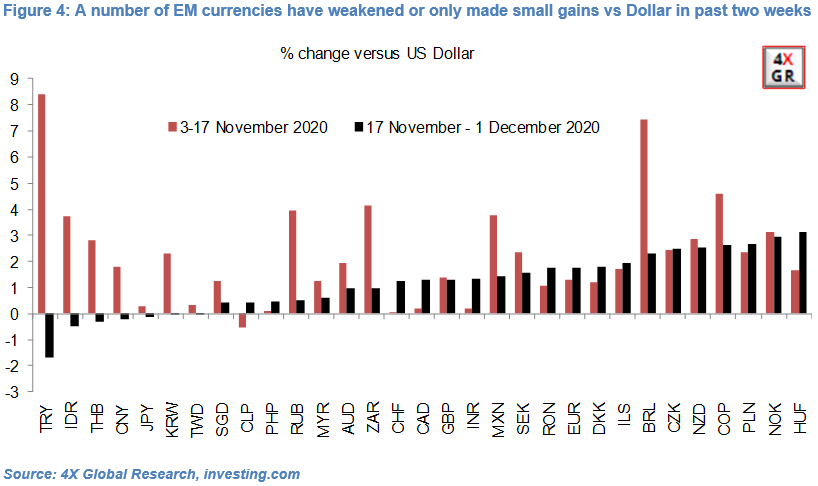

News articles about the November EM currency rally and the long list of factors supporting further outperformance next year have been rife.

EM currencies, particularly high-yielders, materially outperformed in the fortnight following the US elections thanks in part to a pick-up in portfolio inflows. The prevailing view was/is that a less conflictual Biden presidency will be a net positive for global trade and commodity prices. EM currencies appreciated further following news on 23rd November that the more affordable Astra Zeneca vaccine was up to 90% effective and Trump’s announcement that he would allow the transition of power to President-elect Biden.

However, in the past two weeks a GDP-weighted basket of EM currencies (excluding the Chinese Renminbi) has appreciated only 0.9% versus the Dollar and underperformed a basket of developed market currencies (+1.3%). Moreover, high yielding EM currencies (+1.1%) have only marginally outperformed low-yielding EM currencies (+0.7%).

Domestic and regional factors over-and-above “global risk appetite” have arguably contributed to the outperformance of Central European and Latam currencies and the more mixed (read subdued) performance of high-yielding EM and Asian currencies. One explanation is that some of these EM currencies are already pricing in a lot of “good” news.

The consensus forecast is seemingly that EM currencies will outperform both the Dollar and developed market currencies going forward. The long list of supporting factors includes i) cheap EM valuations, ii) EM currencies’ yield advantage, iii) the benefits to EM of further Dollar depreciation and iv) a rebound in global economic growth.

We sympathise with this view, albeit with some important caveats. One is that more interventionist Asian central banks may stop their currencies from fully joining any EM currency party in 2021. Moreover, we would split the next 13 months into three timelines.

Read the full article here

Olivier is an economist and rates & FX strategist with over 22 years experience in financial markets. He is Director and Founder of 4X Global Research, an independent, London-based consultancy which provides institutional and corporate clients with substantive research, high-quality analysis and insight on emerging and G20 economies and financial markets.