What you may have missed and why it matters

Financial-market post-mortems for 2019 are out and the bottom line is that the trade was to be long pretty much everything – including US and global equities, bonds and commodities (bar natural gas) – but short equity and FX volatility.

Trading FX last year was indeed an exercise in both patience and timing with depressed currency volatility going hand-in-hand with trading ranges in most Dollar-crosses – in particular USD/TRY, USD/IDR, and USD/INR – narrowing sharply compared to 2018. The Chilean Peso was the notable exception, with political and civil unrest generating wild swings in USD/CLP.

These themes have broadly held true since the US and China three weeks ago agreed to a Phase One trade deal which they will reportedly sign on 15th January.

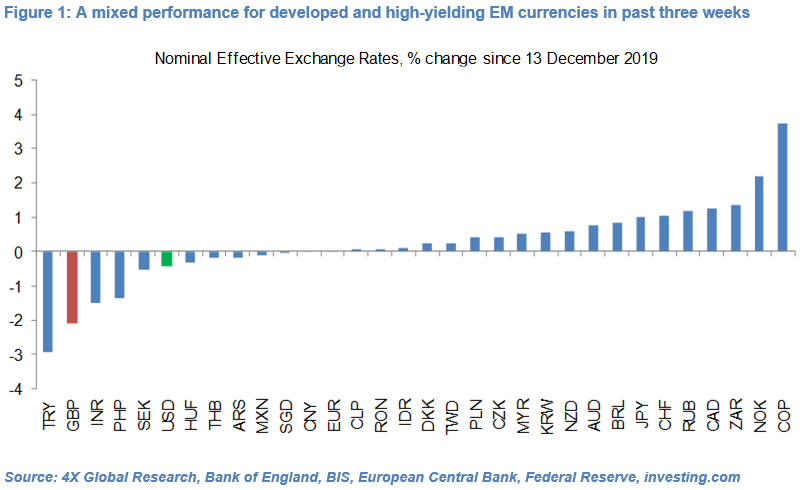

US equities have consistently hit new record highs, including on the first trading day of the New Year, and Latin American currencies and the high-yielding South African Rand have outperformed (see Figure 1).

However, the risk-sensitive Turkish Lira has dropped 3% while the safe-haven Japanese Yen and Swiss Franc have both appreciated 1% and the price of gold has surged 4.4% to a four-month high.

Moreover, the price of Brent crude oil, which was broadly stable in the second half of December, has spiked 4.5% in the past 24 hours, as has the S&P 500 VIX, in the wake of a deadly US air strike in Iraq on Iran’s military commander, General Qasem Soleimani.

The Dollar – on a downward trend since early September – hit a five month low on the last day of 2019 but in the past 24 hours has rebounded 0.4% as markets digest the possible implications of the US killing General Qasem Soleimani on neutral soil. US macro data have been mixed in the past fortnight and the Atlanta Fed GDPNow model, as of 23rd December, estimates annualised GDP growth in Q4 at 2.3% qoq, up slightly from 2.1% in Q3.

Sterling, which is down about 2% since its post general election spike, continues to surf unpredictable Brexit waves and a domestic economy which remained weak in Q4.

Read the full article here

Olivier is an economist and rates & FX strategist with over 22 years experience in financial markets. He is Director and Founder of 4X Global Research, an independent, London-based consultancy which provides institutional and corporate clients with substantive research, high-quality analysis and insight on emerging and G20 economies and financial markets.