Major economies & currencies – What to look out for and why it matters

Price action in major currencies was again subdued last week. With few tier-one macro data releases for markets to trade off the focus was on the reaction function of governments and central banks to covid-19 related developments.

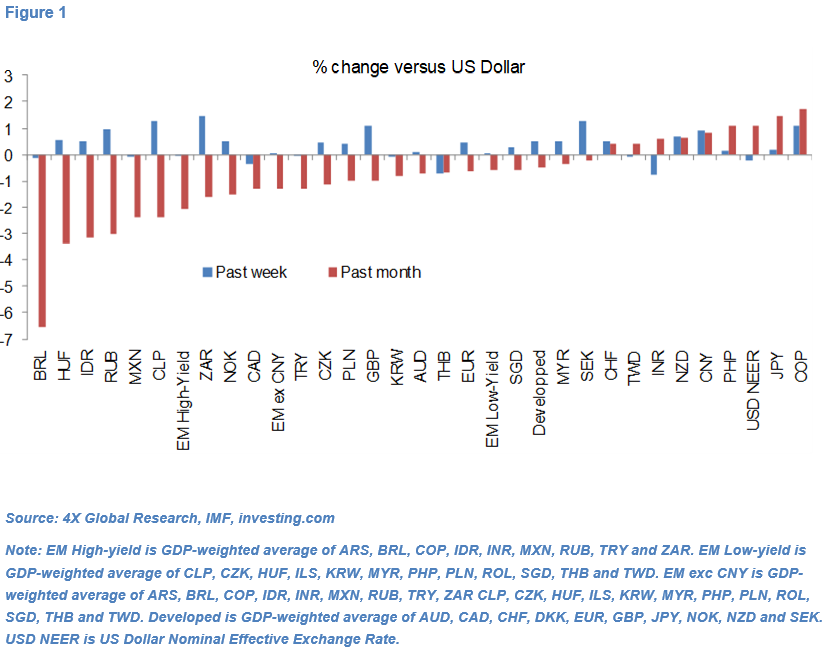

Only a handful of currencies appreciated by more than 1% vs the Dollar last week and no major currency depreciated by more than 0.7%. The net result was that the Dollar Nominal Effective Exchange Rate was down only 0.2% and it is broadly unchanged since Friday.

The calendar for tier-one macro data releases and policy events is far heavier this week, particularly in the US, China and UK. OPEC+ is also due to meet on 15th July with expectations that it will announce plans to start increasing oil production.

Since its rally in mid-June the Dollar has arguably been trading like a “safe-haven” again, with stronger-than-expected US macro data still mostly benefiting US and global equities. In this context this week’s release of June retail sales figures and NY and Philly Fed manufacturing indices for July will be in markets’ eye-sight.

The Sterling NEER is near a one-month high as the British government once again opens the spending taps but UK GDP, inflation, labour market and retail sales data out this week may well put a floor under reasonably high currency volatility.

In the Eurozone, macro data are likely to continue to play second fiddle to pan-European policy stimulus measures, with the Euro likely to be sensitive to this Thursday’s ECB policy meeting and in particular the special EU Summit on 17-18 July.

The Chinese Renminbi has appreciated a slow but steady 1.7% in the past month but has treaded water in the past four sessions. This week’s sequential June data and Q2 GDP figures could prove a litmus test for the PBoC’s appetite for further currency appreciation.

The Australian and New Zealand Dollars are struggling for clear direction but that is not the case of the Thai Baht which, in line with our expectations, has been weakening in July.

Read the full article here

Olivier is an economist and rates & FX strategist with over 22 years experience in financial markets. He is Director and Founder of 4X Global Research, an independent, London-based consultancy which provides institutional and corporate clients with substantive research, high-quality analysis and insight on emerging and G20 economies and financial markets.