Warnings about US economy and USD overblown

The United States’ post-war record GDP contraction in Q2 of 9.5% qoq and the Dollar’s recent depreciation have been making headline news but some perspective is required.

The US GDP contracted about 10.6% in H1 2020, far more than in China (+0.6%) and South Korea (-4.6%). However, of other economies which have so far released Q2 data – including the Eurozone’s four largest economies, Mexico and Singapore – all posted larger rates of contractions in H1 2020. The UK’s GDP likely shrunk more than twice as much whilst France (-19.0%) and Mexico (-18.3%) fared only marginally better.

Moreover, GDP in the US outperformed in H1 2020 despite GDP growth in 2019 (+2.4%) being materially stronger than in Mexico (-0.1%), Italy (+0.3%), Germany (+0.6%), Singapore (+0.7%), the United Kingdom (+1.5%), France (+1.5%) and Spain (+2.0%).

How major economies will perform in Q3 in the context of a rise in the number of local or national covid-19 cases and some countries having (partially) frozen or re-tightened national lockdowns is up for debate. The outlook for Q4, which for Western countries will mean colder weather and a potential increase in covid-19 cases, is even more uncertain.

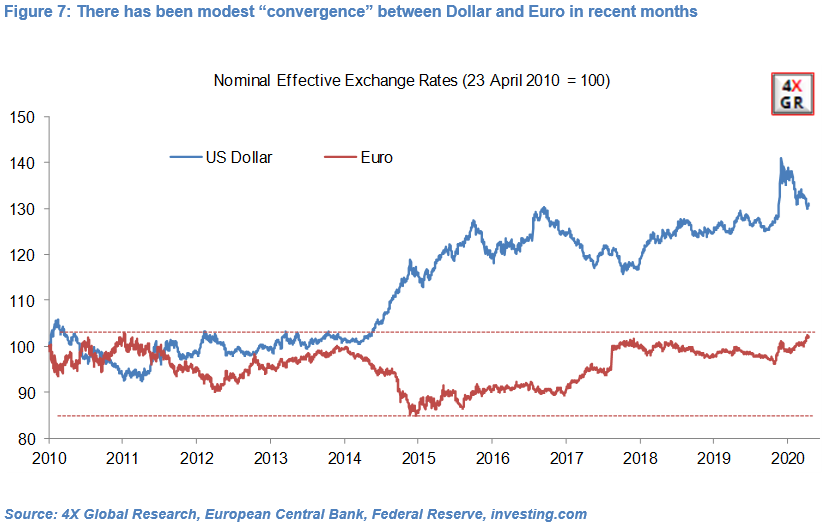

The Dollar’s depreciation in the past six weeks from a strong level is mainly due to successful central bank policies to address imbalances in its supply and demand and a cyclical rotation out of Dollars into other FX reserve currencies, including the Euro.

As a result, the share of Dollars in the world’s central bank FX reserves, which has hovered around 62% in the past two years, may have fallen slightly in recent months while the share of Euros (20%), Sterling (4.4%) and Swiss Franc (0.15%) may have increased marginally.

However, we do not think that FX price action in the past couple of months, including the Euro’s appreciation to multi-year highs, points to the beginning of a structural and permanent shift in the currency composition of central banks’ FX reserves.

In the same way that apocalyptic forecasts in the past about the Eurozone and Euro have failed to materialise, current forecasts of the Dollar’s demise as the world’s number one reserve currency are at best extremely premature, at worst unfounded in our view.

The Dollar’s recent depreciation and United States’ post-war record GDP contraction in Q2 have been making headline news with some analysts already predicating the demise of the Dollar as a reserve currency. We would argue that such forecasts have little basis and that some perspective is required.

Read the full article here

Olivier is an economist and rates & FX strategist with over 22 years experience in financial markets. He is Director and Founder of 4X Global Research, an independent, London-based consultancy which provides institutional and corporate clients with substantive research, high-quality analysis and insight on emerging and G20 economies and financial markets.