Sterling’s made its mind up, UK voters not quite

Sterling has appreciated 1.5% in Nominal Effective Exchange Rate terms since 26th November to a 7-month high, a notable move in a world of depressed currency volatility.

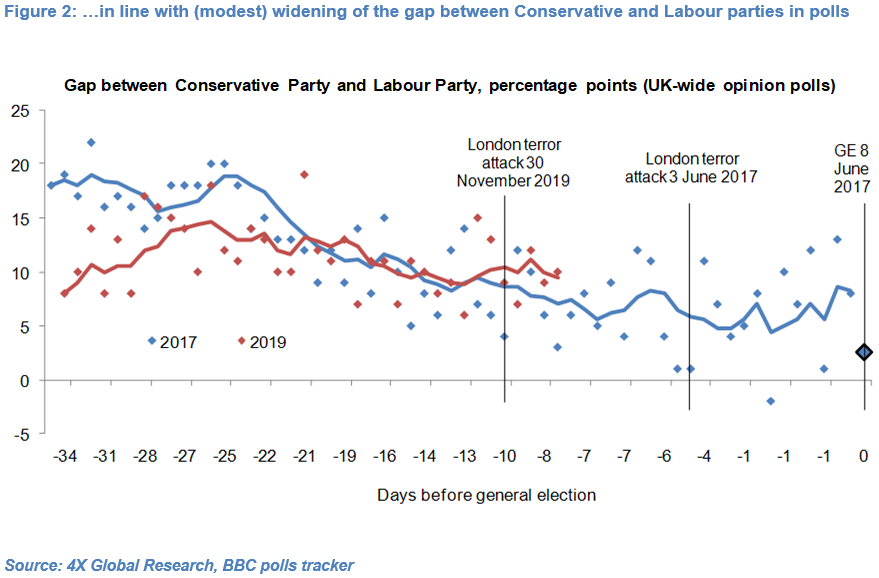

Markets have seemingly taken comfort from the (modest) widening of the gap between the ruling Conservative Party and opposition Labour party in opinion polls to about 10pp and YouGov predicting that Prime Minister Johnson would secure a material parliamentary majority at the 12th December general election.

Upward revisions to UK composite PMI data for November have also at the margin dispelled the notion that UK GDP growth may have contracted in Q4.

Importantly, opinions polls taken in early December 2019 suggest that the gap in support for the two main parties is wider than the 8pp gap which separated the Conservatives and Labour eight days before the 8th June 2017 general election at which the Conservative Party lost its parliamentary majority (see Figure 2).

However, the first-past-the-post electoral system, uneven distribution across seats of candidates – including over 200 independent candidates – party-alliances and tactical voting by the British electorate make it very difficult to accurately translate UK-wide polls into actual seat numbers. The 8th June 2017 general elections are a point in hand.

The odds of the Labour Party winning the most seats and forming a government remain extremely low, in our view. However, the odds of the Conservative Party wining the most seats but failing to win a majority, let alone a material one, remain non-negligible.

In this scenario, we would expect speculative short-Sterling positions to increase materially and in turn weaken Sterling, as was the case between mid-April and mid-August, with markets becoming more sensitive to UK macro data, the possibility of a Bank of England policy rate cut and the risk of the UK leaving the EU without a deal on 31st January.

Read the full article here

Olivier is an economist and rates & FX strategist with over 22 years experience in financial markets. He is Director and Founder of 4X Global Research, an independent, London-based consultancy which provides institutional and corporate clients with substantive research, high-quality analysis and insight on emerging and G20 economies and financial markets.