Shape of Recovery: Square Root & Hockey Stick

While GDP data for Q1 are now “old” and seemingly of limited use, it makes little sense to forecast global growth in Q2 and beyond without at least knowing the starting point.

We estimate, based on data for 19 major economies, that global GDP growth slowed to

-2.6% yoy in Q1 from +3.0% yoy in Q4 2019 and to -4.3% qoq from +0.6% qoq in Q4. Of these 19 major economies only Chile recorded positive quarter-on-quarter growth in Q1.

The outlook for Q2 and beyond is clouded by the unpredictable interplay between the:

1) Complex mathematics and science behind the spread of the covid-19 pandemic;

2) Often unprecedented measures which governments have taken to contain the pandemic, including national lockdowns varied in their length, scope and efficacy;

3) Multiplication of policy measures designed to mitigate the slump in global growth;

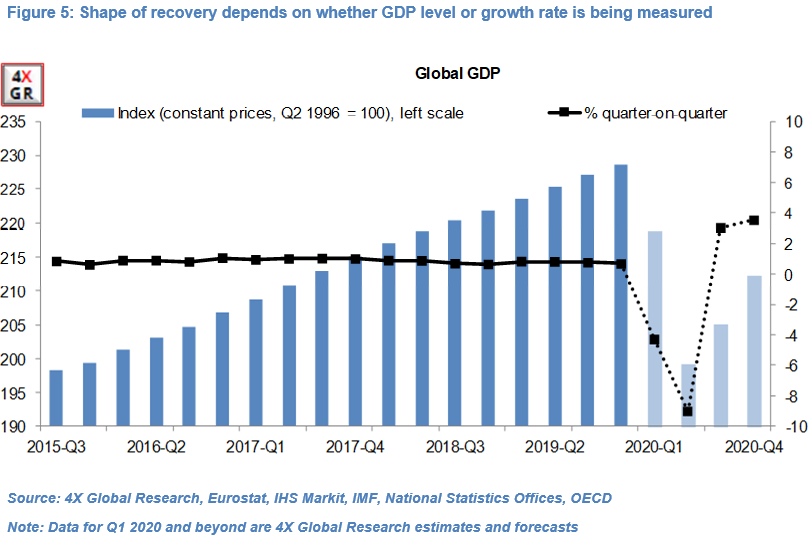

Nevertheless, the consensus forecast for Q2, which we share, is that global GDP will likely contract even more sharply than in Q1. We forecast, based partly on the fall in the global PMI Composite Output index in April-May, that global GDP will contract 9% qoq in Q2, with most major economies in recession. This would imply that global GDP in Q2 will be similar to that of Q4 2015 and that four years’ worth of growth was wiped out in H1 2020.

We forecast global GDP growth in Q3 and Q4 at respectively +3.0% qoq and +3.5% qoq, and to resemble that of a square-root. Our core scenario is that most national lockdowns will continue to be eased and that widespread central bank policy rate cuts in the past year will have a lagged, positive impact on borrowing, expenditure and investment.

In level terms this implies that GDP’s path will be asymmetric, with its recovery in H2 2020 far more modest than its collapse in H1 2020, and will resemble that of a hockey stick. We estimate that GDP in Q4 would be at a similar level as three years prior.

We have some sympathy with the view that global GDP (level) may follow a W-shaped path (in the event of a “second wave” of covid-19 cases) but attribute low odds of a U and in particular L-shaped recovery (i.e. a depression rather than a recession).

Read the full article here

Olivier is an economist and rates & FX strategist with over 22 years experience in financial markets. He is Director and Founder of 4X Global Research, an independent, London-based consultancy which provides institutional and corporate clients with substantive research, high-quality analysis and insight on emerging and G20 economies and financial markets.