National economic recessions – The price to pay

The consensus forecast is that GDP contracted in many major economies in Q1 and will most definitely contract in Q2 as a result of the negative impact of national lockdowns on supply and demand.

The implication is that these economies will be in recession – defined at a country level as two consecutive quarters of negative quarter-on-quarter GDP growth.

A number of major economies, including Japan, France, Italy and South Africa, already recorded negative GDP growth rates in Q4 2019 and may therefore have already been in recession in Q1 2020.

Quarterly GDP data are typically released with a lag of at least a month and so we turn to other key macro variables, released weekly or monthly, to ascertain the magnitude of the current economic downturn.

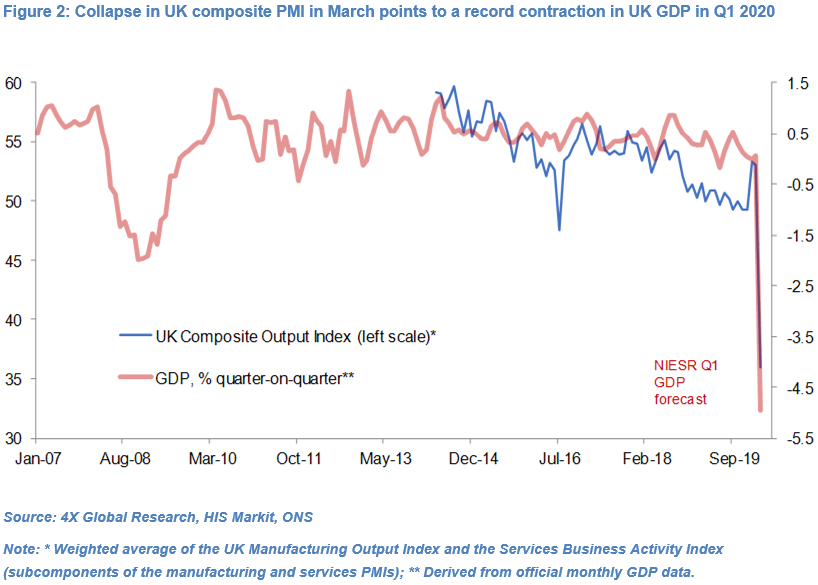

In the United Kingdom, the collapse in the Composite PMI in March gives credibility to the National Institute of Economic & Social Research forecast that GDP shrank 5.0% quarter-on-quarter in Q1. To put this in context the largest quarterly contraction during the Great Financial Crisis was “only” 2.1% qoq (in Q4 2008).

In the United States, the Atlanta Federal Reserve’s GDPNow tracker, a running estimate of the seasonally-adjusted annualised rate of US GDP growth in Q1 based on available data, stood at 1.0% qoq on 9th April.

This number will likely be further revised downwards following the release of other key March data, including retail sales and industrial output (on 15th April), durable goods orders (24th April), goods trade balance (28th April) as well as housing data.

The US Conference Board’s core scenario, which is certainly not the most bearish, is that US GDP will shrink 5.8% qoq in Q1 and by a third in Q2 – three times more than at any other time since World War Two.

Read the full article here

Olivier is an economist and rates & FX strategist with over 22 years experience in financial markets. He is Director and Founder of 4X Global Research, an independent, London-based consultancy which provides institutional and corporate clients with substantive research, high-quality analysis and insight on emerging and G20 economies and financial markets.