EM currencies: Central bank friends and foes

The Fed updated “dot-chart” of all FOMC members’ expectations of the appropriate policy rate points to only an incrementally less dovish stance. Based on a weighted average FOMC members still only expect one 25bp hike by end-2023, according to our estimates.

Fed seems eager to cool market concerns that it will have no choice but to start hiking rates and to ultimately cap Treasury yields or at least slow recent increase in long-end yields. Price action in 2 and 5-year Treasuries suggests it partly succeeded, even if briefly.

However, this still very dovish Fed policy rate outlook jars with its updated forecasts for US inflation and particularly GDP growth. The Fed’s twin arguments are that rapid growth this year will not be very inflationary due to slack in labour market and that following a period of inflation-undershoot it’s willing to accept a modest overshoot in PCE-inflation above 2%.

The latter will have come as little surprise. The more contentious issue in our view is the Fed’s prognosis that core PCE-inflation will rise only modestly from 1.5% yoy in January to 2.2% yoy by end-year despite US GDP growth hitting a 37-year high of 6.5% this year.

The Treasury yield curves have steepened further in the past 72 hours. This suggests that bond markets are not convinced about the Fed’s macro/policy matrix or that the Fed’s pick-up in Treasury purchases in the past couple of months will prove sufficient.

Moreover, the 6.9% collapse in crude oil price yesterday and correction in US equities (particularly the more risk-sensitive Nasdaq) are clear pointers that markets remain concerned about the impact of higher US yields on global demand and equity valuations.

FX markets have been more sanguine. Global FX volatility has risen in past 72 hours but remains in line with 10-year average and most currencies, particularly in Asia, have moved little. The safe-haven Dollar has proven relatively resilient, in line with our February view.

While the Russian Rouble has (perhaps unsurprisingly) weakened most, most other high-yielding emerging market currencies have outperformed, thanks in large part to greater-than-expected central bank rate hikes in Brazil and Turkey of respectively 75bp and 200bp.

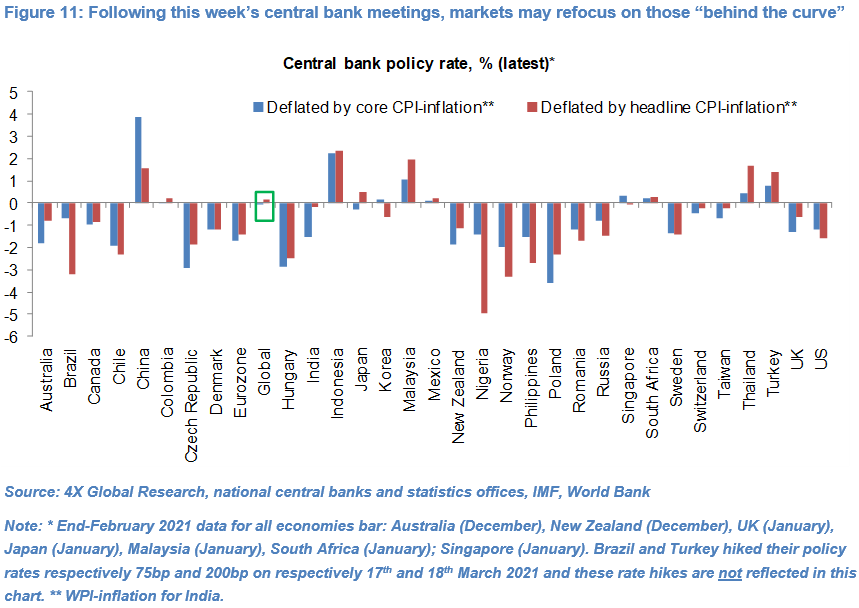

The risk now is that markets redouble their attention on central banks perceived as being “behind the curve”. These include the Norges Bank and CE3 central banks in our view.

Read the full article here

Olivier is an economist and rates & FX strategist with over 22 years experience in financial markets. He is Director and Founder of 4X Global Research, an independent, London-based consultancy which provides institutional and corporate clients with substantive research, high-quality analysis and insight on emerging and G20 economies and financial markets.