Chinese Renminbi – Canary in the coal mine

While the United States and China have not gone as far as re-introducing or increasing tariffs on each others’ imports, the war of words between the two trading superpowers has clearly escalated with Hong Kong caught in the middle.

In line with our expectations the Chinese Renminbi has depreciated versus (a weaker) Dollar and in nominal effective exchange rate terms in recent weeks (see Figures 1 & 2).

Precedent suggests the Renminbi’s slide to an 11-week low is not coincidental but the by-product of the PBoC’s conscious decision to modestly weaken its currency and send a clear, if subtle message to the United States that China can retaliate in more ways than one.

The implications of a breakdown in US-China relations and a resumption of a full-blown trade war would of course reach far beyond a possible acceleration in the pace of Renminbi depreciation.

For starters any sustained Renminbi weakness would likely increase the odds of other Asian currencies also depreciating versus the Dollar with hands-on central banks keen to maintain their countries’ export competitiveness, particularly at this current juncture.

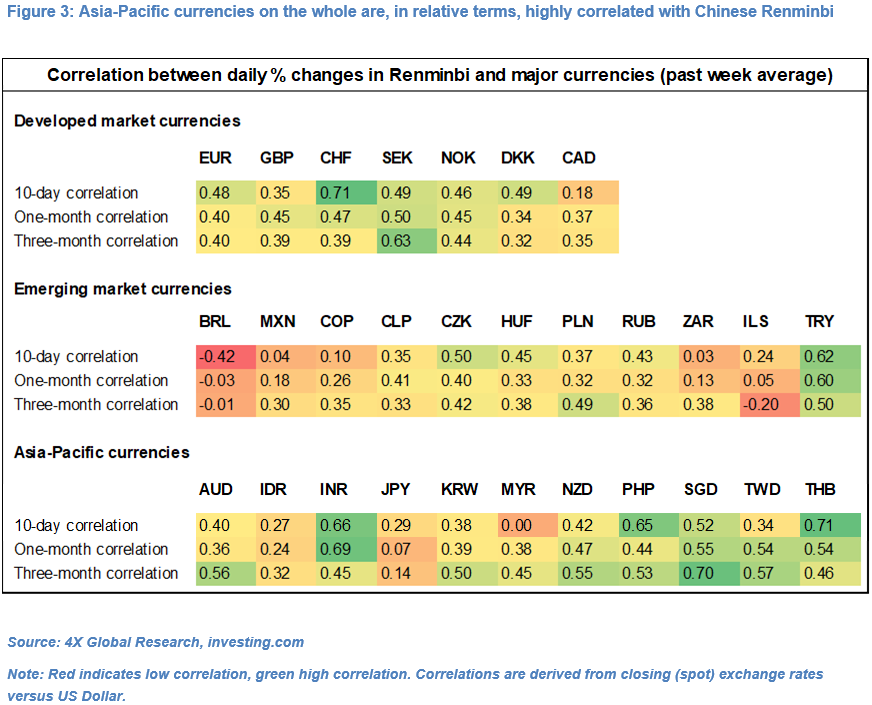

It is no coincidence, in our view, that Asian currencies on the whole remain highly correlated with the Renminbi and have underperformed since 7th May (see Figures 3 & 4).

Moreover, the introduction of new import tariffs would, based on precedent, likely have a material and negative impact on world trade at a time when macro data suggest that global economic activity has only just started to very slowly recover from a very low base.

Any further headwind to global trade would likely delay any meaningful recovery in global supply and demand (see Figure 5) and cast further doubts on whether sequential global GDP growth can forge a V-shaped recovery in Q3 and Q4 2020 – the topic of our next Fixed Income Research & Macro Strategy report.

Read the full article here

Olivier is an economist and rates & FX strategist with over 22 years experience in financial markets. He is Director and Founder of 4X Global Research, an independent, London-based consultancy which provides institutional and corporate clients with substantive research, high-quality analysis and insight on emerging and G20 economies and financial markets.