Central banks to the rescue…with a lag

We have consistently and correctly forecast since October that the 60bp increase in the global central bank policy rate in 2018 would, with a lag, contribute to global GDP growth falling below 3% in 2019 and to lower inflation and that as a result “policy rate cuts, which had all but disappeared since Spring 2018, may resurface in the second half of 2019”.

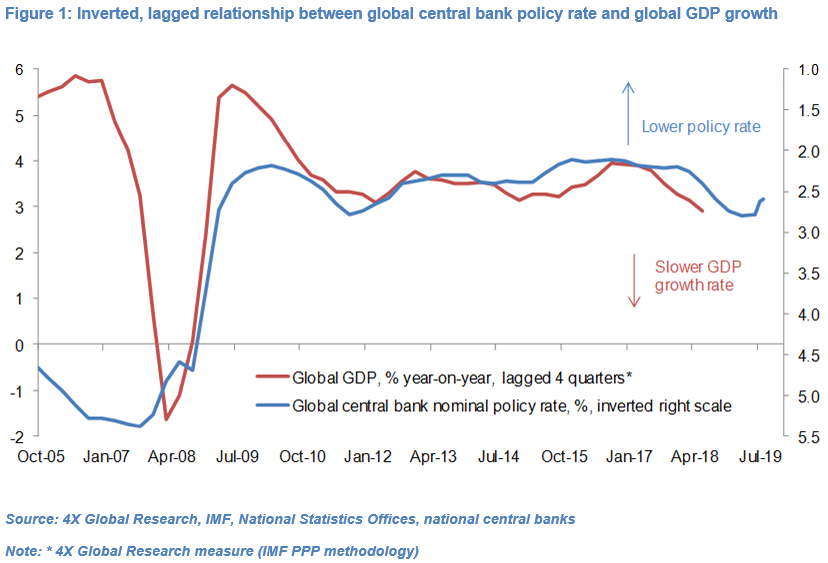

Global GDP growth slowed to a decade low of about 2.9% yoy in Q2 and will, based on lead indicators (including the global manufacturing PMI), likely slow further in Q3 but avoid going into recession. Our measures of global headline and core CPI-inflation – weighted averages of inflation in 30 major developed and EM economies – fell by about 80bp and 25bp, respectively, between October 2018 (the high since April 2012) and July 2019.

Since early May, central banks in Australia, Brazil, Chile, India, Indonesia, Korea, Malaysia, New Zealand, Mexico, the Philippines, Russia, South Africa, Thailand and the US have cut their policy rates. Our measure of the global central bank policy rate, which had been stable around 2.80% between December and May, has since fallen 20bp to 2.60%.

The European Central Bank has left its policy rates unchanged but ECB President Draghi has repeatedly indicated that weak Eurozone growth and inflation may justify policy rate cuts and/or a resumption of its quantitative easing program.

Our analysis shows an inverted, 4-quarter lagged relationship between the global central bank (nominal) policy rate and global GDP growth (see Figure 1). If this historical relationship holds going forward, we would expect GDP growth to slow further in Q3 and Q4, before stabilising in H1 2020 and slowly recovering in H2 2020.

The sustained fall in global GDP growth and inflation this year, and threat posed going forward by the US-China trade war, in our view justifies the easing of central bank interest rate policy in the past four months and amounts to more than just a crude “currency war”.

If anything, central banks should have perhaps started cutting their policy rates sooner and more aggressively (and governments loosened fiscal policy). In any case, we expect central banks, including the Federal Reserve, to cut rates further in the remainder of the year.

This is a summary – Read the full research piece here

Olivier is an economist and rates & FX strategist with over 22 years experience in financial markets. He is Director and Founder of 4X Global Research, an independent, London-based consultancy which provides institutional and corporate clients with substantive research, high-quality analysis and insight on emerging and G20 economies and financial markets.