Brazen ECB verbal intervention against Euro unwarranted and unlikely

Markets bereft of key macro data releases and policy events in recent days will be turning their attention tomorrow to the European Central Bank’s policy meeting.

The consensus forecast, which we share, is that the ECB will leave its policy rates, including its deposit rate (-0.50%), and the modalities of its PEPP and APP unchanged.

However, unnamed ECB Governing Council members in the past week have alluded to the Euro’s appreciation, particularly against the Dollar, and its negative impact on Eurozone exports, economic growth and inflation. This has prompted speculation that the ECB will resort to verbal intervention to weaken the Euro.

Our core scenario is that the ECB will not explicitly try to jawbone the Euro weaker.

We think its policy statement (due out 12.45 London time) will make no reference to the Euro and only likely reiterate the ECB’s commitment “to stand ready to adjust all of its instruments, as appropriate, to ensure that inflation moves towards its aim in a sustained manner, in line with its commitment to symmetry”. At a stretch the ECB may announce a step-up in its monthly APP asset purchases (currently running at €20bn).

President Lagarde may in her introductory press conference statement (13.30) try to short-circuit any temptation for financial markets to push the Euro higher but this would at most constitute verbal intervention “light”.

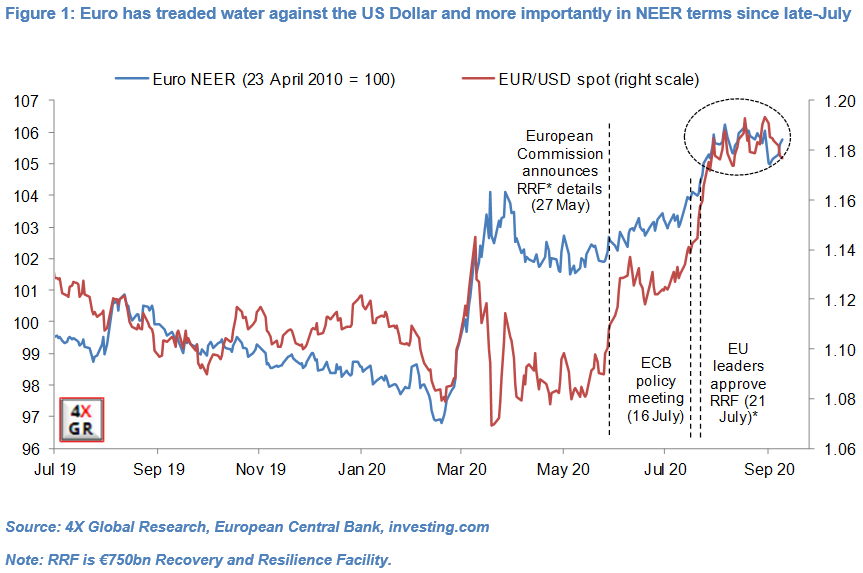

Our main argument is that the Euro Nominal Effective Exchange Rate (NEER) has only appreciated 1.8% since the ECB’s last policy meeting on 16th July and has thus had a negligible deflationary impact. Moreover, the Euro’s rise occurred in the second half of July, following EU leaders’ approval of the €750bn Recovery and Resilience Facility. Since then the Euro has treaded water in NEER terms (and against the US Dollar).

Moreover, based on precedent, we think the ECB will privilege low Euro volatility over specific Euro exchange rate levels.

Read the full article here

Olivier is an economist and rates & FX strategist with over 22 years experience in financial markets. He is Director and Founder of 4X Global Research, an independent, London-based consultancy which provides institutional and corporate clients with substantive research, high-quality analysis and insight on emerging and G20 economies and financial markets.