United Kingdom: Back to 1999… and to the future

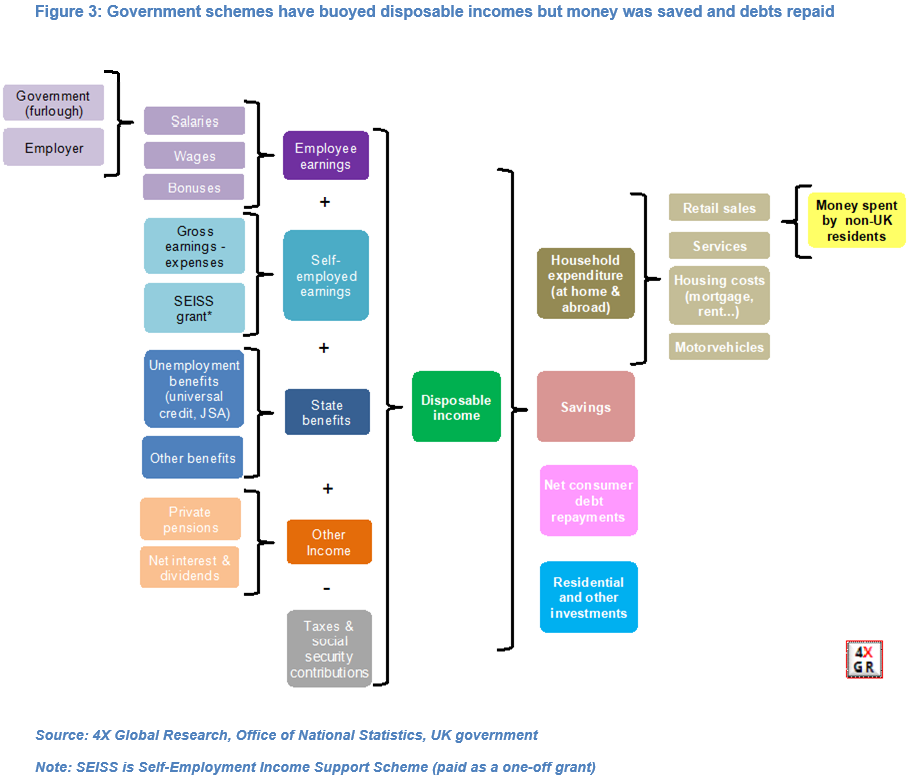

Part Two of this Five-part series of Insights into the UK economy and financial markets examines the critical role played by the British government, which continues to pump tens of billions into the economy via a vast array of measures, including a furlough scheme, to support household disposable incomes and ultimately consumption and GDP growth.

Households’ limited opportunities to spend, rather than the acute drop in consumer confidence and constraints on purchasing power, was the main cause behind the fall in domestic consumption in March-April and record collapse in GDP. Retail sales indeed fell far more sharply than implied by the historical correlation with consumer confidence.

More importantly the £46bn (32%) collapse in household spending on goods and services in April – equivalent to a staggering 25% of monthly GDP – dwarfed the (at worst modest) fall in households’ disposable incomes. Aggregate worker earnings fell by only £2bn (2.8%) in April, mainly thanks to the government’s furlough scheme, and access to state benefits (including universal credit) was eased.

GDP growth was awful in April, merely bad in May. We estimate that it contracted “only” 3% mom to levels not seen since 1999. The composite PMI rebounded to 30 from an all-time low of 13.8 in April, the value of retail sales rose 12% and households may have withdrawn some of their sizeable cash deposits and/or curtailed their debt repayments. However, the labour market continued to deteriorate and the services sector remained in stasis.

We forecast that GDP growth hit a record-high 10% mom in June, as a result of both “favourable” base effects and a rebound in economic activity, implying that GDP in Q2 contracted a record 23% qoq. There were greater opportunities to spend as the lockdown was eased and self-employed workers accessed the income support scheme in size.

Our core scenario is that UK GDP growth will accelerate to about 10% qoq in Q3 and 15% qoq in Q4, which would imply GDP contracting about 11.5% in 2020. It is premised on our expectations that the lockdown will continue to be eased gradually and that household incomes, savings and consumer confidence will fuel consumption and headline growth.

Read the full article here

Olivier is an economist and rates & FX strategist with over 22 years experience in financial markets. He is Director and Founder of 4X Global Research, an independent, London-based consultancy which provides institutional and corporate clients with substantive research, high-quality analysis and insight on emerging and G20 economies and financial markets.