The key quartet: US income, confidence, net worth and consumption

In US Consumer – From King to Prince (8 October 2019), we argued that “the recent fall in US consumer confidence, slowdown in income and wage growth and jitters in US equity markets suggest that Personal Consumption Expenditure (PCE) growth remained weak in September and thus slowed materially in Q3” (September data are due on 31st October).

Weak September retail sales data, released on 16th October, support that view given the strong, positive historical correlation between the volume of retail sales and real PCE.

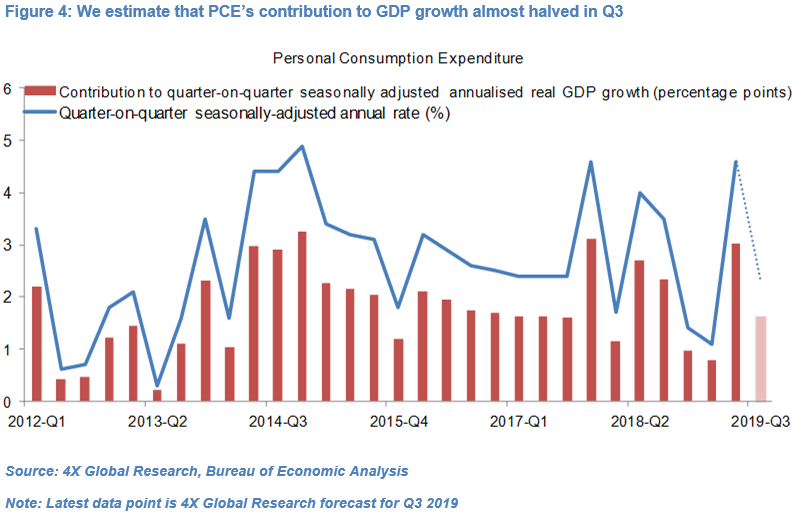

We estimate that the quarter-on-quarter SAAR of real growth in PCE halved to 2.3% from 4.6% which would imply that PCE growth in Q3 contributed only 1.6 percentage points to headline GDP growth, a little more than half of the 3.0pp it contributed in Q2 (see Figure 4).

The risk therefore is clearly biased towards GDP growth having slowed further in Q3 from 2.0% qoq in Q2. Note that the advance estimate of Q3 GDP is due out on 30th October at 13.30 (London time), only hours before the Federal Reserve concludes its policy meeting.

Forecasting PCE growth is complex as it is driven by a significant number of inter-related and often self-reinforcing factors. Yet our detailed analysis shows a strong, positive historical correlation between disposable income (including wages & salaries), US consumer confidence, households’ net-worth (including equity holdings), and PCE.

The slowdown in disposable income growth this year (due to weaker growth in “other incomes” and rising tax take), rising share of disposable income saved and recent fall in US consumer confidence do not bode well for PCE growth in Q4 and beyond.

However, the $7.2 trn rise in households’ net assets in H1 2019 and US equity markets’ resilience near record-highs should support consumer confidence and suggest that PCE and US GDP growth will remain positive, if modest, near-term.

This may not stop the Federal Reserve from cutting its policy rate 25bp once more before year-end, but the market’s current pricing of 30bp of rate cuts between now and-2019 looks a touch over-done, in our view.

This is a summary – Read the full research piece here

Olivier is an economist and rates & FX strategist with over 22 years experience in financial markets. He is Director and Founder of 4X Global Research, an independent, London-based consultancy which provides institutional and corporate clients with substantive research, high-quality analysis and insight on emerging and G20 economies and financial markets.