Non-Japan Asia: NEERs and FX intervention

Non-Japan Asian (NJA) central banks’ foreign currency (FX) reserves have gradually increased since end-March 2020, arguably the peak in global risk aversion.

We estimate that the aggregate US Dollar-value of FX reserves in China, India, Indonesia, Korea, Malaysia, Philippines, Singapore, Taiwan and Thailand increased by about $514bn or 10% in the eleven months to end-February 2021 to about $5.66 trillion. This was just $122bn short of all the all-time high recorded in June-2014.

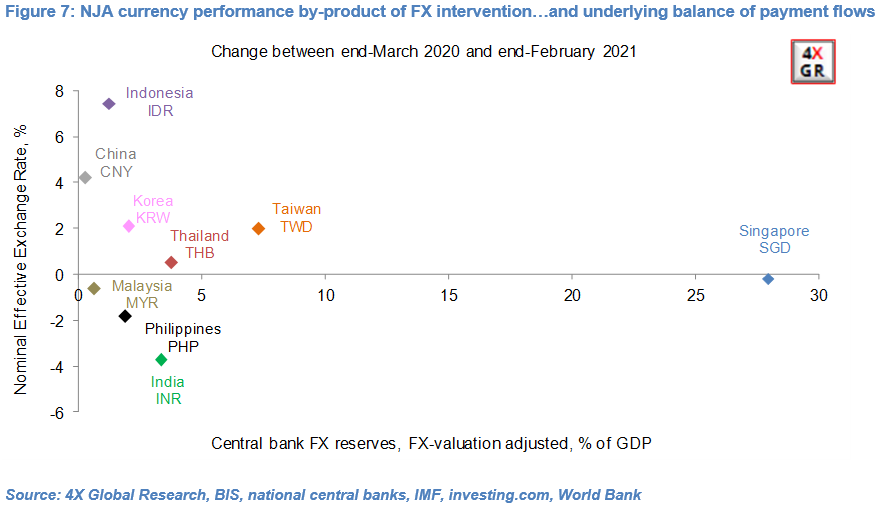

Adjusting for currency-valuation effects – the appreciation of other major reserve currencies versus the US Dollar – we estimate that these NJA central banks’ FX reserves increased by about $342bn or 6.4%. As a percentage of GDP, this increase amounted to about 1.5% for NJA, ranging from only 0.3% in China to nearly 28% in Singapore.

While realised investment gains on these central banks’ holdings and other official transactions may have inflated this increase in FX reserves, it was at least partly the result of central banks’ intervention in the FX market (i.e. buying foreign currency), in our view.

Importantly, NJA central banks rightly attach greater importance to their currencies’ more relevant Nominal Effective Exchange Rates (NEERs), when setting their exchange rate and interest rate policies, than to their currency’s bilateral exchange rates, in our view.

In the past 11 months NJA central banks have continued to show an ability and willingness to both limit daily FX volatility and influence their NEERs’ medium-term directionality.

FX reserve accumulation has either capped the pace of appreciation (CNY, IDR, KRW, THB, TWD) or contributed to (albeit modest in most cases) NEER depreciation (INR, MYR, PHP) with NJA central banks seemingly intent on maintaining export competitiveness and limiting imported deflation. The Singapore Dollar NEER was unchanged over this period.

Of course the past and future performance of individual currencies is conditioned by both the magnitude of central bank FX intervention AND current account and capital account flows (and the underlying factors behind these policies and FX flows) – the topic of Part Two of this FIRMS report.

Read the full article here

Olivier is an economist and rates & FX strategist with over 22 years experience in financial markets. He is Director and Founder of 4X Global Research, an independent, London-based consultancy which provides institutional and corporate clients with substantive research, high-quality analysis and insight on emerging and G20 economies and financial markets.