Governments and policies adapting to critical known unknown

We argued in Lack of US market & macro volatility both reassuring and troubling (17 January) that “the market’s willingness to look through domestic political and geopolitical events suggests that only a significant exogenous or endogenous shock currently beyond markets’ radar screens (an “unknown unknown”) is likely to really move the needle”.

That unknown unknown, a “black swan” event, has turned out to be a global viral pandemic on a scale not seen since the Spanish influenza pandemic of 1918-1919.

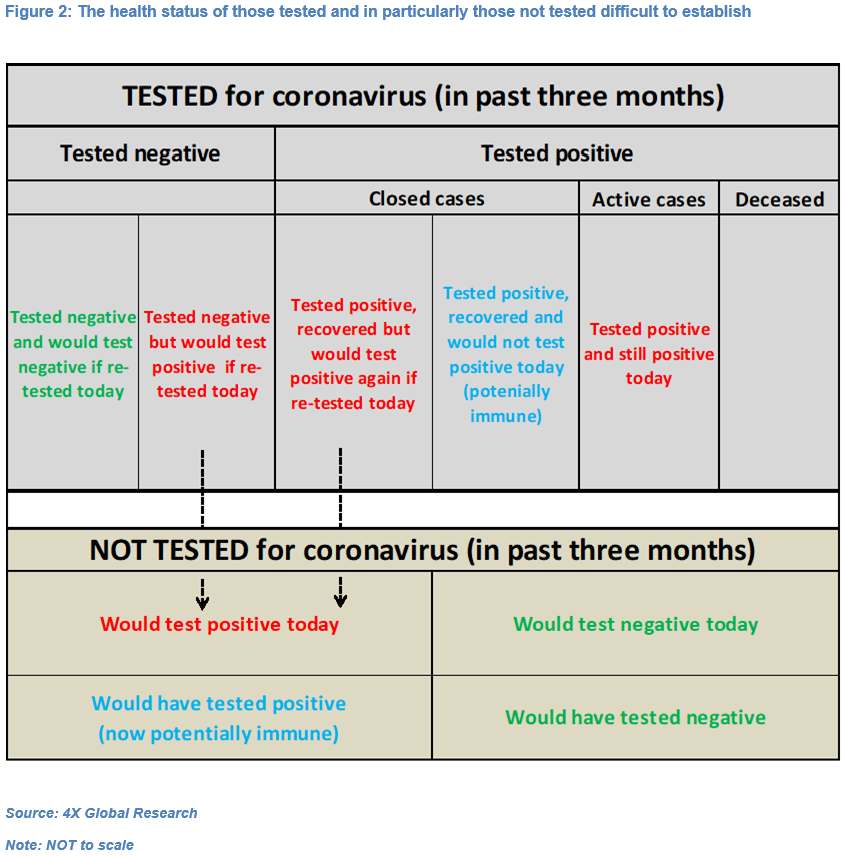

The coronavirus outbreak is now three months old but governments, central banks, corporates and households still face a critical known unknown, in our view, namely the total number people who 1) had the coronavirus, acquired immunity and are no longer contagious and 2) currently carry the coronavirus and are thus potentially infectious.

This includes people who have not been clinically tested – more than 99.9% of the world’s population. We estimate that only 3.3 million people (4 out of every 10,000) have been tested for coronavirus, although testing data are patchy and often released with a lag. The main reason so few people have been tested is the still limited capacity to rapidly and reliably test a very large number of people.

In econometric terms that is a very small sample from which to extrapolate country-wide trends. One implication is that the actual mortality rate may be far smaller than reported.

The high number of tests-per-capita conducted in countries such as South Korea has been posited as an explanation for their relatively low number of coronavirus-related deaths. However, other factors have likely been at play, including the timing of clinical tests, demographics, national health systems’ capacity to treat infected patients and the timing and efficacy of self-isolation and self-distancing policies, including country “lockdowns”.

For now what policy-makers know they don’t know will likely continue to influence country-specific containment plans, as well as domestic measures to support economic growth while ensuring the functioning of financial markets.

Read the full article here

Olivier is an economist and rates & FX strategist with over 22 years experience in financial markets. He is Director and Founder of 4X Global Research, an independent, London-based consultancy which provides institutional and corporate clients with substantive research, high-quality analysis and insight on emerging and G20 economies and financial markets.