Asian central bank policy rates – scalpel not knife

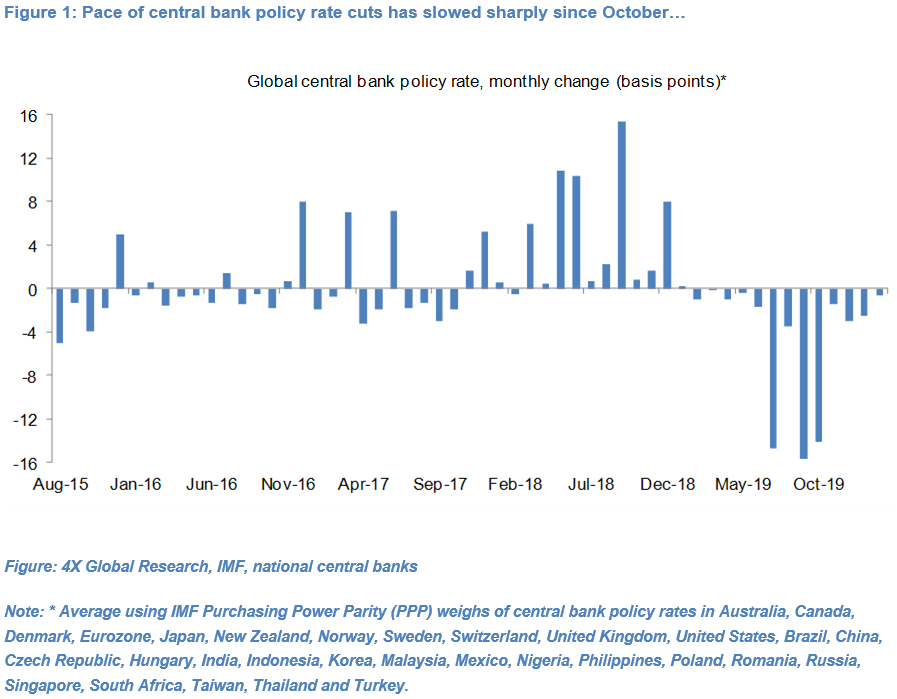

The pace of central bank policy rate cuts has slowed sharply in the past few months (see Figure 1), in line with our view (see Early Christmas for (still weak) global growth, 11th December 2019).

While the emerging market central bank policy rate has fallen a further 20bp since late-October to a multi-decade low of just 4.55%, the developed economy central bank policy rate has been broadly unchanged at around 70bp according to our estimates. In particular the Fed, ECB, BoE, BoJ, RBA and RBNZ have all kept rates on hold.

The extent to which the coronavirus negatively impacts Chinese, regional and global GDP growth will going forward at least partly dictate central banks’ interest rate paths, particularly in Asia-Pacific, and more broadly monetary policy.

Chinese PMI data point to only a modest slowdown in Chinese economic activity in January but they don’t tell the full picture, in our view. Our core scenario at this stage is that global GDP growth, which looked set to pick-up slightly in Q1 2020 from 3.0% yoy in H2 2019, will have slowed to around 2.5% yoy in Q1, its slowest pace in a decade.

We thus think the risk is biased towards Non-Japan Asian (NJA) central banks cutting their policy rates further in coming months. The case for Bank of Indonesia is particularly compelling given slowing CPI-inflation and GDP growth and Rupiah appreciation.

However we think the overall pace and magnitude of policy rate cuts in NJA will be modest, for two reasons.

For starters, most NJA (and EM) central banks have already cut rates aggressively in the past nine months to multi-year lows and may want to see how these rate cuts feed through to domestic growth and inflation before embarking on another round of sustained rate cuts.

Second, the Thai Baht and Korean Won Nominal Effective Exchange Rates (NEERs) have all weakened since the beginning of the year. All other things being equal this equates to a loosening of monetary policy which in turn reduces the Thai and Korean central banks’ need to cut policy rates, in our view.

Read the full article here

Olivier is an economist and rates & FX strategist with over 22 years experience in financial markets. He is Director and Founder of 4X Global Research, an independent, London-based consultancy which provides institutional and corporate clients with substantive research, high-quality analysis and insight on emerging and G20 economies and financial markets.