China’s V-shaped recovery under the microscope

Chinese GDP growth (seasonally-adjusted) was 11.5% qoq in Q2. This was stronger than consensus forecast (+9.6% qoq) and more than reversed Q1 contraction of 9.8% qoq. This record-high growth reflects both a post-lockdown bounce in economic activity and of course extremely “favourable” base effects.

This is pertinent for China but also its key major trading partners and global economy. China accounts for about 20% of world GDP in PPP terms and thus growth single-handedly contributed about 2.3 percentage points to quarter-on-quarter global GDP growth in Q2.

We estimate that in constant terms China’s GDP hit a record high in Q2 2020, was 0.6% larger than in Q4 2019 and only 2.2% lower than if GDP growth had continued to trend at 1.4% qoq. For GDP to return to “trend” in Q3 GDP growth would have to be about 3.7% qoq.

In this scenario the shape of China’s GDP level would approximate that of a square-root (a broadly symmetric recovery). In comparison we expect the recovery in global GDP to resemble that of a hockey-stick (an asymmetric recovery) as most major economies likely contracted sharply in Q2 (Shape of Recovery: Square Root & Hockey Stick, 5 June 2020).

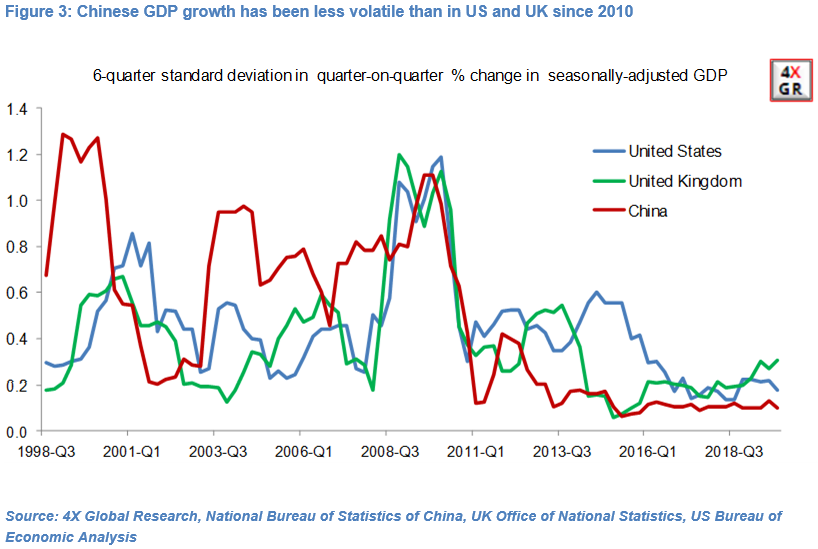

Over the years analysts have queried the accuracy of official Chinese data, with the consensus view seemingly that they overstate the “real” pace of domestic economic growth. This remains difficult to prove (or disprove) in our view.

In the past decade quarterly Chinese GDP growth has been steady and less volatile than in major developed economies, including the United States and United Kingdom, which has led to suggestions that Chinese GDP data are being “smoothed”.

Chinese Policy makers could counter that they have more policy-levers at their disposal than their US and British counterparts and that GDP growth in China was far more volatile in Q1 2020 and likely Q2 than in the United States and United Kingdom.

Our analysis suggests that official GDP data do capture the broad changes in the direction of Chinese economic growth. Notably unofficial manufacturing PMI data have historically correlated more closely with the official GDP than official PMI data have.

Read the full article here

Olivier is an economist and rates & FX strategist with over 22 years experience in financial markets. He is Director and Founder of 4X Global Research, an independent, London-based consultancy which provides institutional and corporate clients with substantive research, high-quality analysis and insight on emerging and G20 economies and financial markets.