Brexit’s (probably) coming home and markets don’t care…for now

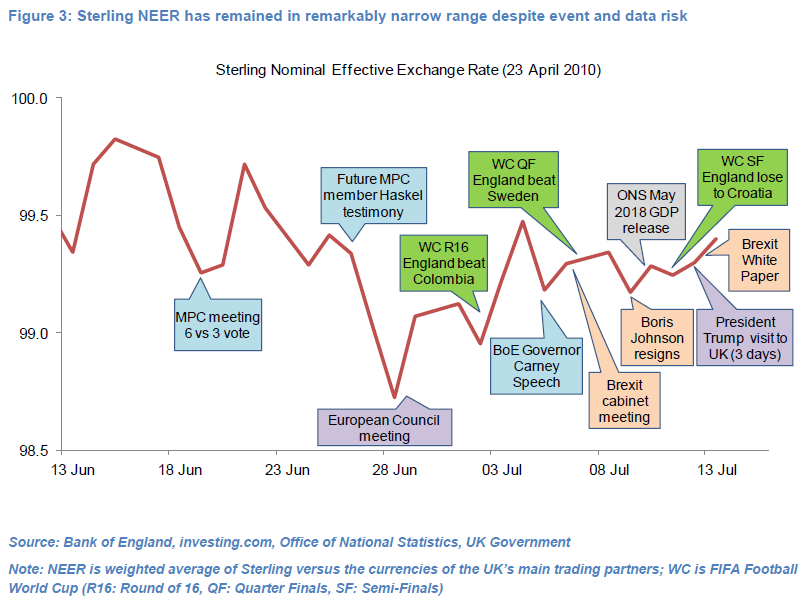

UK financial markets have been remarkably stable in the past month despite having to contend with a plethora of macro data, UK-driven events and global developments.

The FTSE 100 has traded in a narrow 3.4% band since mid-June, market pricing for a rate hike at the Bank of England’s policy meeting on 2nd August has oscillated between 15.5bp and 19bp and, in line with our expectations, Sterling has remained directionless (Sterling caught in growth and Brexit trap, 13 June 2018).

The government’s detailed and much-awaited blueprint for the UK’s relationship with the EU post Brexit, published on 12th July, sets out a vision whereby the UK would remain aligned with the EU on many fronts in exchange for close trading ties.

The receding risk of a Hard-Brexit and recent upturn in economic growth have seemingly put a floor under Sterling but with the domestic political and economic picture still very cloudy markets, which were wrong-footed ahead of the Bank of England meeting on 10th May, are rightly not getting carried away.

Near-term the risk to Sterling is somewhat biased to the downside, in our view.

The market is already pricing in a 75% probability of the Bank of England hiking rates on 2nd August. At the same time a lot of the “good” news regarding Brexit is now in the public domain and the government still faces a number of challenging hurdles in coming months.

In any case Sterling volatility is likely to pick up as we get closer to the October-November deadline for the British and European parliaments to approve a post-Brexit deal.

The “will of the people” and “a price worth paying” has become an unassailable government mantra not just despite evidence that the price has been and will continue to be high but because of tangible evidence that the price may not be worth paying.

Prime Minister Theresa May has only a few months left to prove to the electorate, companies and markets that doctrine and reality can align.

This is a summary – Read the full research piece here

Olivier is an economist and rates & FX strategist with over 22 years experience in financial markets. He is Director and Founder of 4X Global Research, an independent, London-based consultancy which provides institutional and corporate clients with substantive research, high-quality analysis and insight on emerging and G20 economies and financial markets.