US and UK: The Comeback Kids

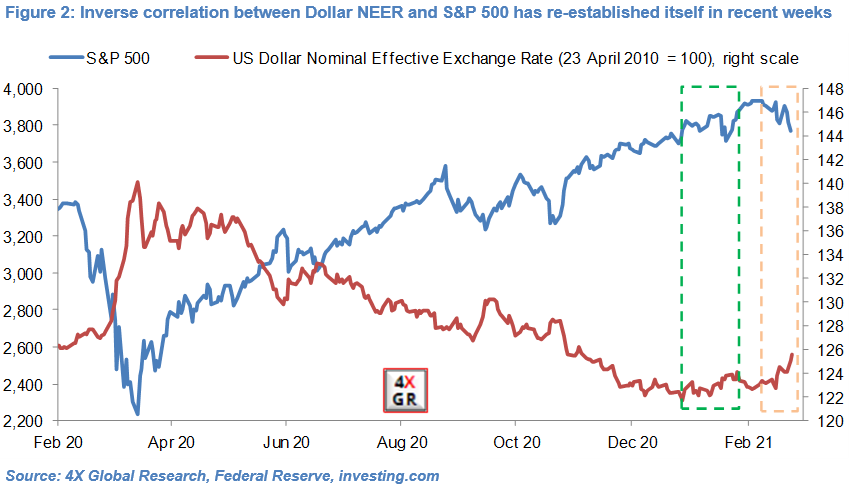

The US Dollar NEER has since 12th February appreciated about 2.3% to a 4-month high and its inverse correlation with the S&P 500 (-4.2%) has re-established itself. This is in line with our forecast that the Dollar’s sell-off in early February was “a small, short-term correction” rather than “another prolonged downtrend”. If anything we were not bullish enough.

We are also sticking with our view “that material Dollar depreciation may not resume for another couple of months, until it becomes clearer that a matrix of loose US fiscal policy but still low US interest rates will dent the Dollar’s attractiveness”.

At the same time we think the slow start of the vaccination process in many major developed and EM economies could delay a meaningful rebound in global confidence and GDP growth and continue to act as a brake for emerging market currencies as a whole.

Macro data indeed point to still weak global growth in early 2021, in our view. However, the significant build-up of private sector savings in developed economies offers the prospect of pent-up demand being unleashed once vaccination programs have matured and governments have materially eased domestic lockdown measures.

Moreover, US economic activity – as measured by income and consumption – recovered in January-February, albeit from a low base, thanks in part to fiscal stimulus measures, a strengthening of the labour market and reasonably loose social distancing measures.

It is early days but so far financial markets’ reaction to British Chancellor of the Exchequer Sunak’s UK Budget announcement on 3rd March 2021 has been pretty tepid.

This is in line with recent years’ budgets, with Sterling, the FTSE 100 and UK Gilts moving little on budget day and in subsequent trading sessions, and in line with our forecast that this year’s “two-pronged transitional” budget would be no different.

We maintain our view that policies largely outside of the Chancellor’s remit – particularly the relative pace of vaccination in the United Kingdom and by extension the likely timeline for a relaxation of still stringent lockdown measures and recovery in domestic economic growth – will continue to drive domestic financial markets, including Sterling.

Read the full article here

Olivier is an economist and rates & FX strategist with over 22 years experience in financial markets. He is Director and Founder of 4X Global Research, an independent, London-based consultancy which provides institutional and corporate clients with substantive research, high-quality analysis and insight on emerging and G20 economies and financial markets.