“Currency wars” not central banks’ end-game

Not a day passes without the media and US President Trump pointing the finger at “currency wars” and “competitive devaluations”.

The thrust of the argument is that central banks across the world, in a “race to the bottom”, are cutting policy rates and in the case of the ECB resuming QE, in order to weaken their currencies and boost export competitiveness and in turn economic growth and inflation. A concern is that these rate cuts are at best pointless and at worst damaging by fuelling the fall in global government bond yields into negative territory.

We have a somewhat more benign interpretation, namely that:

1. The majority central banks have cut their policy rates to boost borrowing, domestic demand and investment, rather than to weaken their currencies per se, in response to slowing domestic and global GDP growth and inflation and to the threat of a further global economic growth slowdown posed by the US-China trade war.

If the end-goal of lower policy rates is indeed weaker (and more competitive) currencies, as often reported, central banks have other and arguably more effective tools, at least in the short-run, such as FX intervention.

2. Ultimately, bar the People’s Bank of China (PBoC), very few central banks have actively engaged in a “currency war”; and

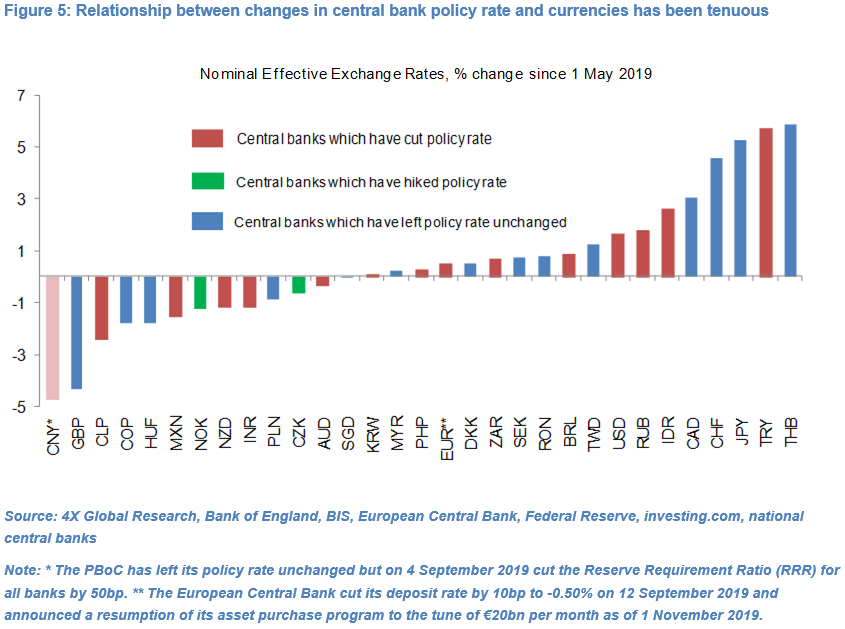

3. There has been limited correlation between countries’ central bank policy rates and the performance of their currencies since the beginning of the easing cycle in early May, suggesting that at the very least “currency wars” have not been very effective (see Figure 5). The inverse correlation between the US-German government bond yield spread and EUR/USD spot exchange rate in the past year is a case in hand.

Central banks may of course welcome a weaker currency as a by-product of a lower (relative) policy rate but the transmission mechanism to currencies and ultimately domestic GDP growth is not particularly compelling.

This is a summary – Read the full research piece here

Olivier is an economist and rates & FX strategist with over 22 years experience in financial markets. He is Director and Founder of 4X Global Research, an independent, London-based consultancy which provides institutional and corporate clients with substantive research, high-quality analysis and insight on emerging and G20 economies and financial markets.